Unseating the Giant

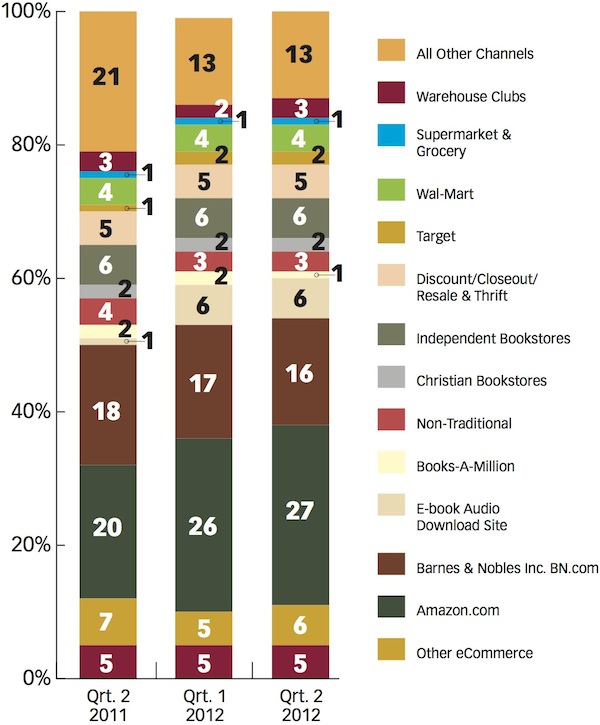

Amazon’s market power is formidable: it’s easily the dominant channel for book revenues with a 27% share of all dollars spent. Like Wal-Mart in the brick-and-mortar world, Amazon can dictate commercial terms to its suppliers. It can unilaterally set price, it can make or break sales forecasts, and it can command whatever margins it wants. It can even afford to lose money on every sale in order to compete.

{kind=link}

And compete it does. Amazon can often independently set the price of the digital products it sells, regardless of cost per unit. It sells many digital products below cost as a customer acquisition and growth strategy, making it nearly impossible for competitors without huge bankrolls to enter the market.

Apple has provided some relief to publishers with its agency terms for iBooks, which allow publishers, rather than Apple, to set the end-user price. Apple simply keeps a cut of what it sells. In 2010, Macmillan single-handedly forced Amazon into those terms with a very public standoff that, luckily for Macmillan, ended in favor of the publisher. But such tactics are within reach of only the biggest publishers, and serve to demonstrate Amazon’s continued prowess as de facto dictator in the world of consumer publishing. (Heck, even the Department of Justice seems to want to protect Amazon’s monopoly position.)

There are umpteen reasons this is bad for everyone. Amazon’s behavior has served to devalue a piece of content in all its forms. I’d argue that a consumer who sees an Amazon Kindle book for $9.99 is disinclined to buy the hardcopy book at retail for $17.99. The net effect–regardless of whether this user is buying from Amazon–is a devaluation of the print product, which remains the main source of revenue for many publishers. In this case, print isn’t shifting to digital: it’s just shrinking, starving publishers of resources for interesting new projects.

And for products that are nonetheless approved, monolithic pricing yields monolithic products. If every bestseller is $9.99, then every bestseller must be engineered by the publisher into a rational P&L that starts with a $9.99 sale price. We can’t have a diversity of digital products in such a narrow band of prices. Product diversity is, alas, the very promise that new technology holds: as a palette for information, the tablet is infinitely more flexible than the printed book.

iBooks can’t help us here because, despite Apple’s best attempts, it is fundamentally undifferentiated. Aside from a handful of handcrafted titles, it offers the same products at similar prices in the same format. It will survive, as Kindle does, on the life support of its deep-pocketed parent, justified as a strategic investment that sells hardware. Nook is less differentiated, and has found pockets in friendly neighbors like Microsoft and Pearson. It just doesn’t seem sustainable.

Now, when I talk about $9.99 prices and commoditized products, I’m talking specifically about immersive text, read front-to-back: the kind of stuff you read on a Kindle. The transition to digital for that kind of content is now decelerating. As of 2012, this only represents about $3 billion of the $14 billion trade publishing industry in the US. So what about the other $11 billion? A huge chunk is more sophisticated (in oh-so-many ways) than 50 Shades of Gray. It’s going to require more sophisticated technology and distribution, and it’s fertile ground for new growth, but the incumbents won’t lead the way.

What keeps Amazon at bay in round two? In a word, product.

The scale-above-all-else mentality that dominates Amazon’s culture is at odds with product innovation. For Amazon, this is not about publishing; it’s about distribution. But when new product models emerge within publishing–ones that set a new consumer expectation for quality and capability–Amazon will be left without the intellectual property to compete. It’s not that Amazon won’t continue to be a dominant distributor of ten-dollar text files; I’m sure they will. But the center of gravity in publishing will shift when publishing product models are diverse, and Amazon can’t support the interesting ones.

Inkling is defining a new product model with media rich, highly structured content that’s reliably rendered across platforms. The technologies we’ve had to develop to do this are far more complex than we’d anticipated when we started the company. Other companies will need to invest years of R&D to achieve the knowledge and technologies Inkling has already acquired or built.

That technology differentiation allows us to build unique products in partnership with publishers. One of our bestselling titles is $200 a copy, and is happily snapped up by users all over the world. Why? Because it’s worth it. Another bestseller is $50 a copy. Consumers will pay for quality when they know they’re getting it. And “quality” isn’t the first word one associates with a Kindle title.

Amazon’s strategy has really dealt a blow to the publishing supply chain that feeds them the content they need. Publishers, in turn, have been constrained in their ability to innovate, working almost exclusively to feed the beast they love to hate. The future is bright, but it won’t be because someone built a better way to sell plain text. It’ll be because a number of innovative companies–Inkling among them–have defined new models for innovative products that render the oligopoly of existing distributors less relevant. New distribution channels and compelling “book” products will establish a second wave in the digital transition.

Odds are, the good stuff won’t be available through Amazon.

About the Author